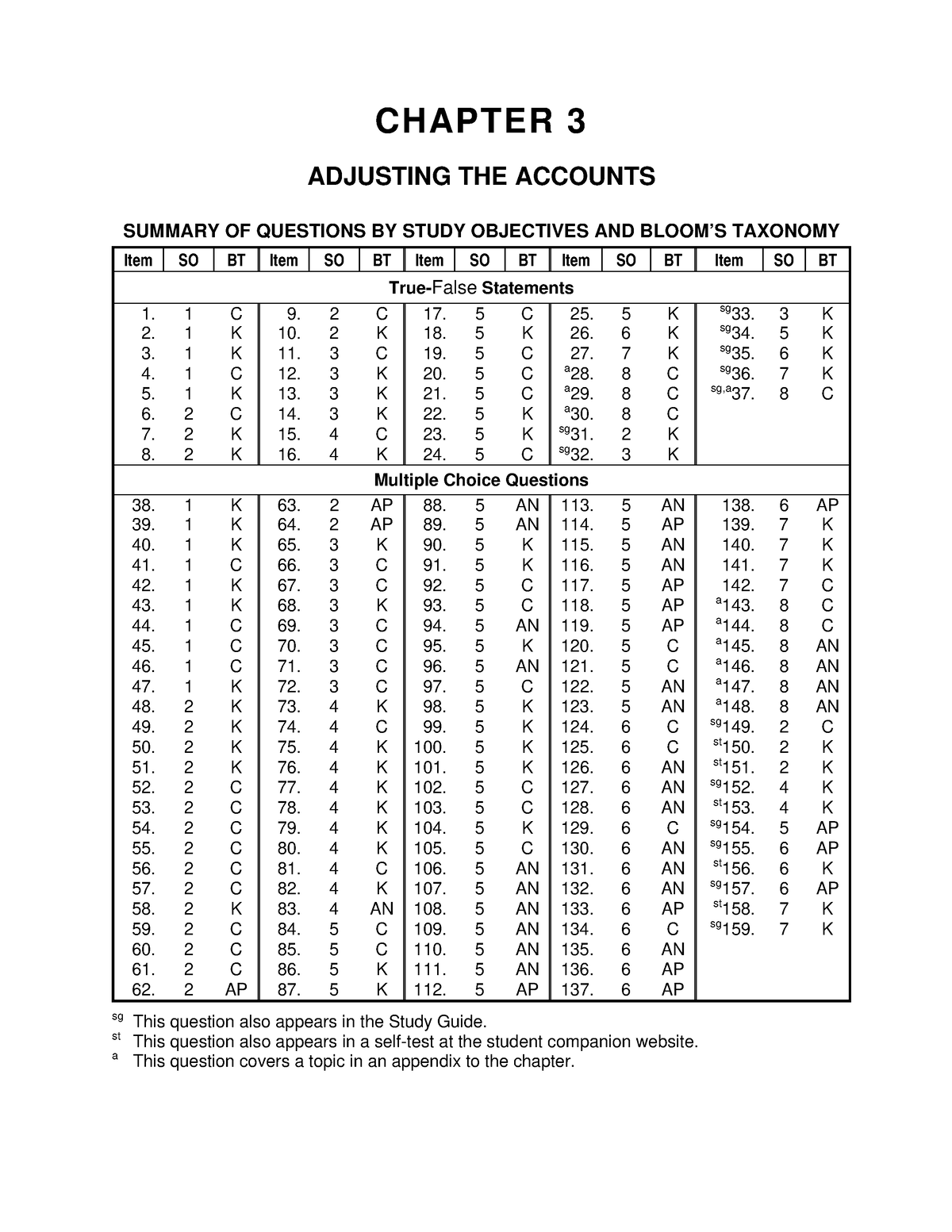

For the past 52 years, Harold Averkamp (CPA, MBA) hasworked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. Press Post and watch your fixed assets automatically depreciate and adjust on their own. We at Deskera offer an intuitive, easy-to-use accounting software you can access from any device with an internet connection. The conference showrunners will pay you $2,000 to deliver a talk on the changing face of the tote bag industry. Adjusting entries will play different roles in your life depending on which type of bookkeeping system you have in place.

Create a Free Account and Ask Any Financial Question

A business may earn revenue from selling a good or service during one accounting period, but not invoice the client or receive payment until a future accounting period. These earned but unrecognized revenues are adjusting entries recognized in accounting as accrued revenues. When you make an adjusting entry, you’re making sure the activities of your business are recorded accurately in time.

Everything to Run Your Business

For example, let’s say a company pays $2,000 for equipment that is supposed to last four years. The company wants to depreciate the asset over those four years equally. This means the asset will lose $500 in value each year ($2,000/four years). In the first year, the company would record the following adjusting entry to show depreciation of the equipment. Supplies increases (debit) for $400, and Cash decreases (credit) for $400. When the company recognizes the supplies usage, the following adjusting entry occurs.

How much will you need each month during retirement?

Overall, adjustment entries play a crucial role in ensuring the accuracy and reliability of financial statements. Companies that take the time to properly record and adjust their accounts will be better equipped to make informed business decisions and meet their financial obligations. Accumulated depreciation is the total amount of depreciation recorded for a long-term asset since it was acquired. To record accumulated depreciation, an adjusting entry is made to increase the accumulated depreciation account and decrease the corresponding asset account.

What is Qualified Business Income?

In simpler terms, depreciation is a way of devaluing objects that last longer than a year, so that they are expensed according to the time that they get used by the business (not when you pay for them). First, during February, when you produce the bags and invoice the client, you record the anticipated income. As your company scales, this is only going to happen more often, meaning you’ll want an effective and efficient way to enter and manage journal adjustments. Say, for example, that your company is a web design agency undertaking a large project that’s expected to take six months to complete. The client pays 20% up front, with the remainder being due on completion.

- Our intuitive software automates the busywork with powerful tools and features designed to help you simplify your financial management and make informed business decisions.

- Press Post and watch your fixed assets automatically depreciate and adjust on their own.

- At the same time, managing accounting data by hand on spreadsheets is an old way of doing business, and prone to a ton of accounting errors.

When you make an adjusting journal entry, you must follow the standard rules of double-entry accounting. An accrued expense, for example, reflects a bill you’ve received but not yet paid. Accrued revenue, on the other hand, reflects invoices you’ve sent to customers for which you’re still waiting on payment.

Cash accounting and accrual accounting are two distinct accounting methods that define when revenue and expenses are recognized. Any business that uses the accrual accounting basis instead of the cash accounting basis will need to make adjusting entries in their general ledger. Another example is to reflect how revenue is earned for long-term projects. The cash hasn’t hit your account yet, so there is no ledger entry for that revenue. But from an accounting perspective — assuming your business uses the accrual basis rather than the cash basis — that revenue has been earned. As a result, there is little distinction between “adjusting entries” and “correcting entries” today.

Want to learn more about recording transactions as debit and credit entries for your small business accounting? By definition, depreciation is the allocation of the cost of a depreciable asset over the course of its useful life. Depreciable assets (also known as fixed assets) are physical objects a business owns that last over one accounting period, such as equipment, furniture, buildings, etc. Accrued expenses are expenses made but that the business hasn’t paid for yet, such as salaries or interest expense.

This also relates to the matching principle where the assets are used during the year and written off after they are used. Accrued expenses and accrued revenues – Many times companies will incur expenses but won’t have to pay for them what is standard cost its an estimate until the next month. Since the expense was incurred in December, it must be recorded in December regardless of whether it was paid or not. In this sense, the expense is accrued or shown as a liability in December until it is paid.

In our example, assume that they do not get paid for this work until the first of the next month. Income Tax Expense increases (debit) and Income Tax Payable increases (credit) for $9,000. Interest Expense increases (debit) and Interest Payable increases (credit) for $300. Accrued expenses are expenses incurred in a period but have yet to be recorded, and no money has been paid. Besides deferrals, other types of adjusting entries include accruals. With the Deskera platform, your entire double-entry bookkeeping (including adjusting entries) can be automated in just a few clicks.

Adjusting entries update previously recorded journal entries, so that revenue and expenses are recognized at the time they occur. Even though you’re paid now, you need to make sure the revenue is recorded in the month you perform the service and actually incur the prepaid expenses. In the accounting cycle, adjusting entries are made prior to preparing a trial balance and generating financial statements. For example, going back to the example above, say your customer called after getting the bill and asked for a 5% discount.